I am 55 years old and would like to know about my retirement options.

I know there are various options such as lump sum withdrawals or changing my retirement annuity to a life or living annuity.

�

Could you please explain the different tax implications of the various options?

�

Also, I was retrenched five years ago and received a R30 000 tax -free contribution in the retrenchment package.

Will this affect the R315 000 tax free benefit of withdrawing my retirement annuity?

Sor� Cloete, senior� legal� manager at Old Mutual, responds:

There are three types of retirement funds:

* Pension funds;

* Provident funds; and

* Retirement annuities.

�

Each of these is governed by a set of rules, the Income Tax Act and the Pension Funds Act, which determine when you may retire from these funds, usually from the age of 55 (like with a retirement annuity).

In the case of a retirement annuity and pension fund, you will only be allowed to take a third of the fund value as a lump sum upon retirement. The balance must provide you with a monthly pension or annuity.

In the case of a provident fund, you may take the full fund value as a lump sum upon retirement.

With a pension and provident fund, you may withdraw from the fund prior to retirement age, but with a retirement annuity you cannot withdraw from the fund prior to retirement age.

�

In addition to the retirement funds mentioned above, we also have preservation funds, where funds are preserved upon resignation until retirement.

�

When retiring from a retirement fund, you are required to purchase an annuity or pension. You will then have the option to either purchase a life annuity or a living annuity.

A life annuity pays a guaranteed income to you, the annuitant (person who will receive the annuity) until you pass away. The annuity then ends and the capital is lost unless a guaranteed term has been placed on the annuity.

With a life annuity, you can also add an option that the income is paid to you until you die and then to your spouse until he/she dies.

With a living annuity, your funds are invested and you may draw an income of between 2.5% and 17.5% of the capital value of the assets in the fund.

The amount drawn from a living annuity can be reviewed on an annual basis. The type of annuity selected will depend on your circumstances.

�

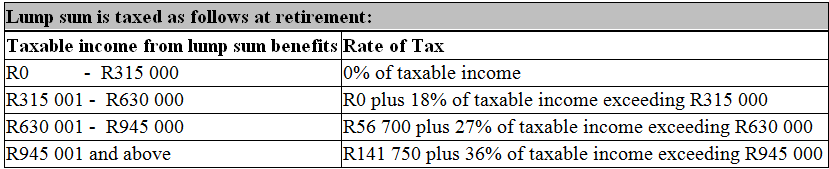

Tax implications on lump sums from retirement funds

�

Upon retirement from a retirement fund, your taxable lump sum will be taxed according to the following table:

�

�

To determine your taxable lump sum from your retirement fund, the following amounts may be deducted:

* Contributions you made to the retirement fund that did not previously rank as an income tax deduction;

* Any amount previously taxed in terms of a divorce award;

* Certain amounts transferred from a government employee�s pension fund;

* Any amount taxed previously when transferring from one retirement fund to another.

�

Where a taxpayer has received lump sums before, the lump sum received upon retirement will be taxed as follows:

Step 1: The current taxable lump sum is determined, which includes lump sums from retirement funds and severance/retrenchment benefits;

Step 2: Add the following benefits received before:

* Taxable lump sums received from retirement funds upon retirement as from Oct 1 2007;

* Taxable lump sums received from retirement funds� upon withdrawal as from March 1 2009;

* Severance/retrenchment benefits received as from March 1 2011.

Step 3: Add the lump sums in step 1 and step 2;

Step 4: Calculate the tax payable on the total calculated in step 3 as per the table above;

Step 5: Calculate the tax payable on the total calculated in step 2 as per the table above;

Step 6: Tax payable = Tax calculated in step 4 less tax calculated in step 5.

�

You indicated that you received a retrenchment benefit five years ago.

If we assume that this was prior to March 2011, then such a benefit will be ignored when calculating the tax payable on the lump sum that you receive now. �

�

Should you however withdraw from a retirement fund, then a different tax table will apply:

�

�

The same principles as discussed in terms of retirement will apply upon withdrawal when calculating the tax payable.

�

The information provided above is only of a general nature and it is advised that you should consult with an expert, like a financial adviser or broker in terms of all your options available upon retirement from a retirement fund.

�

The taxable explanations are quite technical. Please let me know if you need any more information.

– Fin24